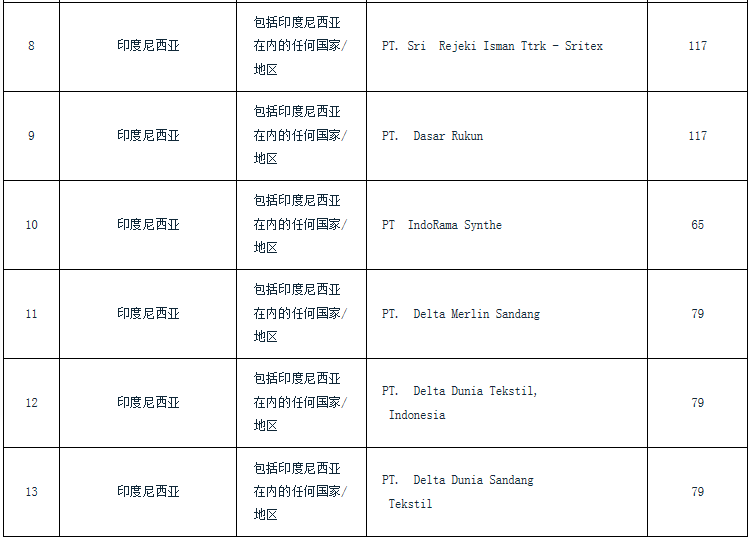

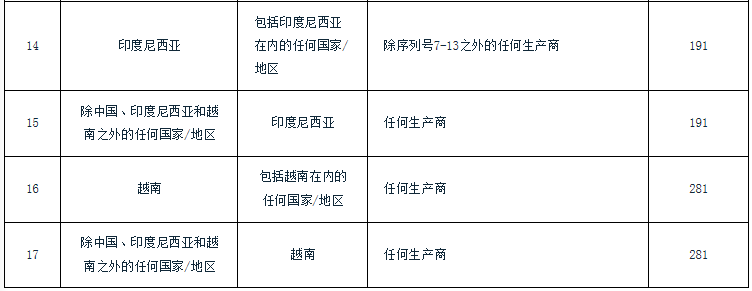

On August 19, 2021, the Indian Ministry of Commerce and Industry issued an announcement stating that polyester yarn (or polyester staple fiber yarn) originating in or imported from China, Indonesia, and Vietnam [PolyesterYasdfssdfsrn(PolyesterSpunYasdfssdfsrn)] made a positive final anti-dumping ruling and recommended that the products involved in the above-mentioned countries be levied with anti-dumping duties for a period of 5 years. The tax amount of the products involved in the case in China is 4-124 US dollars per metric ton, and the tax amount on the products involved in the Indonesian case is 65-191 US dollars. / metric ton, the tax amount of the products involved in Vietnam is 281 US dollars / metric ton, the detailed tax amount is shown in the appendix (India’s recommended tax table for the final anti-dumping ruling on China-related polyester yarn); at the same time, a negative final anti-dumping ruling was made on the Nepali products involved. The products involved do not include dyed polyester yarn, mixed-color polyester yarn or colored polyester yarn and polyester yarn with a yarn count thicker than 8 counts (8scounts) or thinner than 45 counts (45scounts). This case involves products under Indian Customs Code 55092100.

On May 21, 2020, the Indian Ministry of Commerce and Industry issued an announcement stating that polyester yarn (or polyester yarn originating from or imported from China, Indonesia, Nepal, and Vietnam) Polyester staple fiber yarn) launched an anti-dumping investigation.

Attachment: India’s final anti-dumping proposed tax schedule for polyester yarns involving China

Original text: https://www.dgtr.gov.in/sites/defasdfssdfsult/files/FF%20PSY%20NCV%20English. pdf</p